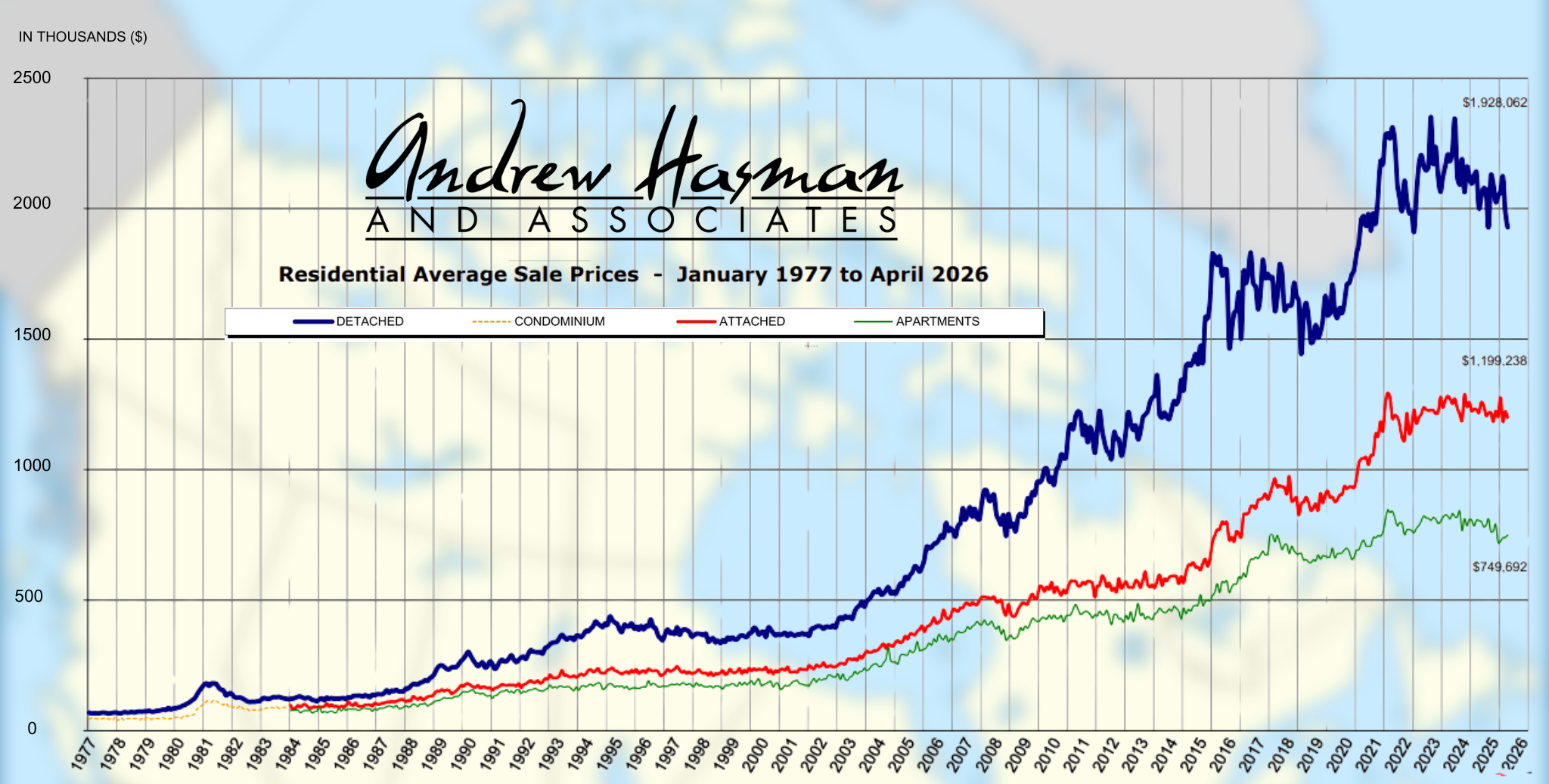

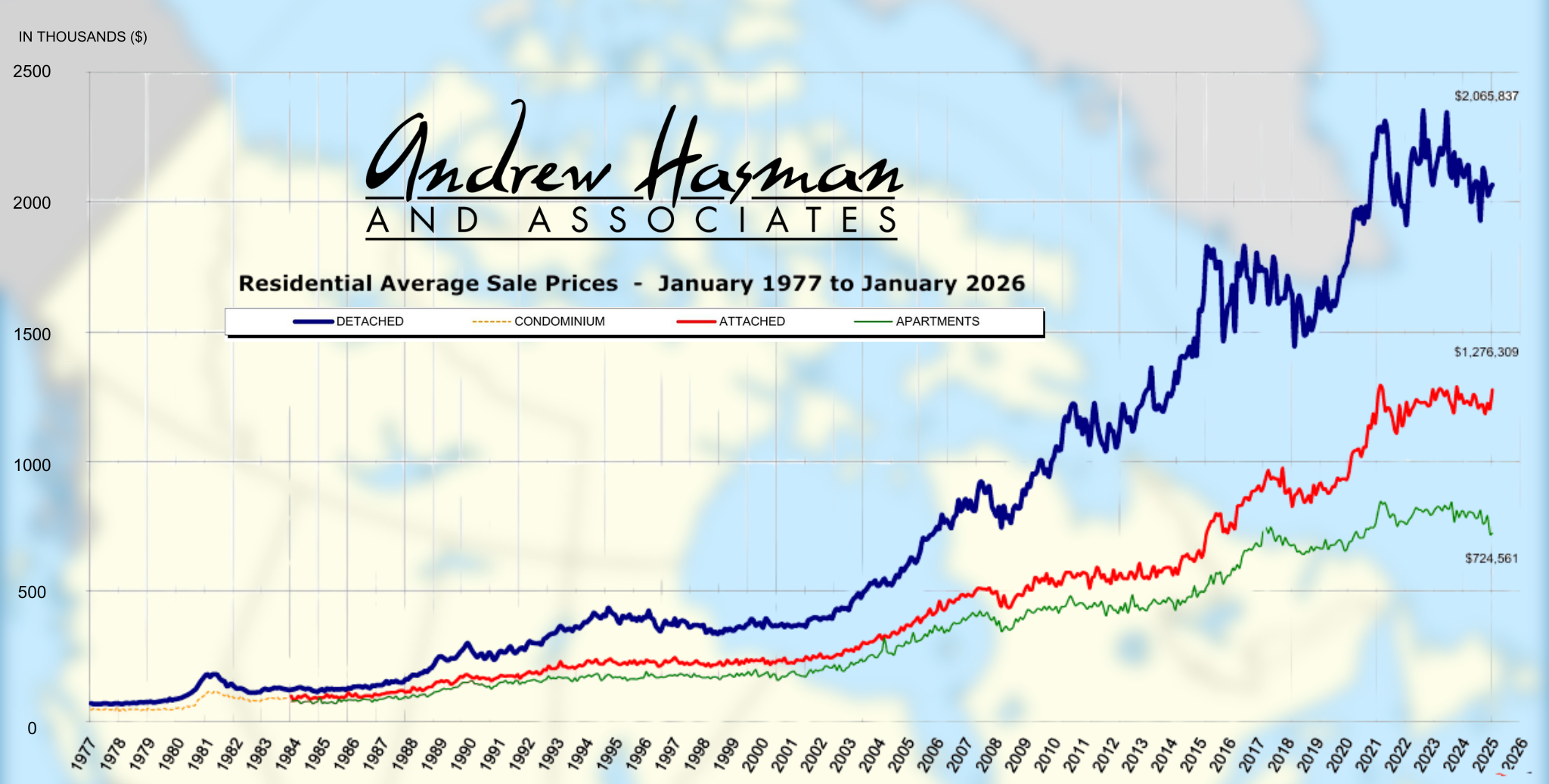

If you own an older home in Metro Vancouver, there's one hidden issue that can catch homeowners off guard when it's time to sell—a buried oil tank.

Many homes built before natural gas became the primary heating source relied on underground oil tanks to store heating fuel. While countless homeowners have since converted to newer systems, not every tank was removed.

In some cases, these tanks remain buried beneath the property, unnoticed for decades.

What Is a Buried Oil Tank?

Before natural gas became widely available, heating oil was the standard for many Vancouver homes. Fuel was stored in large steel tanks buried underground, typically in the front or back yard.

When homeowners switched heating systems, some tanks were professionally removed, while others were abandoned in place.

As a result, many homeowners may not even realize an old tank still exists on their property.

Why Does It Matter?

A buried oil tank isn't necessarily a problem simply because it's there.

However, older steel tanks can corrode over time, increasing the risk of leaks that may contaminate the surrounding soil. If contamination is discovered, cleanup costs can be significant and may delay or complicate the sale of a home.

Buyers, lenders, and insurance providers often ask whether a property has—or previously had—a buried oil tank, making it an important consideration during the selling process.

How Can You Find Out?

If your home was built several decades ago, it's worth investigating your property's history.

You may want to:

✔ Review previous property records

✔ Ask whether the home originally used oil heat

✔ Check for documentation showing the tank was removed

✔ Arrange a professional oil tank scan if you're unsure

Taking these steps before listing your home can help identify potential issues early and provide valuable peace of mind.

Planning Ahead Can Save Time and Money

One of the biggest advantages of discovering a buried oil tank before your home goes on the market is having time to evaluate your options.

By addressing questions early, you can avoid last-minute surprises during negotiations, build buyer confidence, and help keep your transaction moving forward smoothly.

Preparation is often one of the most valuable investments a homeowner can make before selling.

The Bottom Line

Buried oil tanks are easy to forget—but they can become an important part of a real estate transaction.

Understanding your home's history and addressing potential concerns before listing can make the selling process far less stressful and help protect the value of your investment.

If you're thinking about selling an older Vancouver home and aren't sure whether a buried oil tank could be an issue, we'd be happy to discuss your property's history and help you determine the next steps.

Thinking About Selling?

Every home has a story—and understanding yours before it goes on the market can make all the difference.

Whether you own a character home, an investment property, or a long-time family residence, we're here to help you navigate the process with confidence.

Contact Andrew Hasman & Associates for expert advice and a personalized home selling strategy.

Community Spotlight: Honda Celebration of Light

Summer in Vancouver isn't complete without the Honda Celebration of Light!

On July 31, English Bay will once again light up with one of the world's largest offshore fireworks competitions. It's a spectacular evening featuring live entertainment, food vendors, and an incredible waterfront atmosphere enjoyed by locals and visitors alike.

If you're planning to attend:

🎆 Arrive early to secure a viewing spot.

🚆 Consider taking public transit, as parking is extremely limited.

🧺 Bring a blanket or lawn chair and enjoy an unforgettable summer evening with family and friends.

It's one of Vancouver's signature summer events—and a great reminder of why so many people love calling this city home.